🗣 Monthly Update for May 2026

Here’s what we published this month across FinTech Feed and FinGTM — including our latest ecosystem guide and two deep-dive playbooks on B2B lending, lending infrastructure, and vendor selection.

Welcome back to FinTech Feed’s monthly check-in, where we recap what we’ve published and point you toward the most valuable insights for fintech operators, founders, revenue leaders, product teams, and infrastructure builders.

Quick reminder on how this all fits together:

FinTech Feed — our free newsletter covering fintech trends, infrastructure, market shifts, and go-to-market strategy.

FinGTM — our paid companion publication with execution-grade playbooks, vendor breakdowns, frameworks, and tactical guidance for operators, founders, and revenue teams building in fintech.

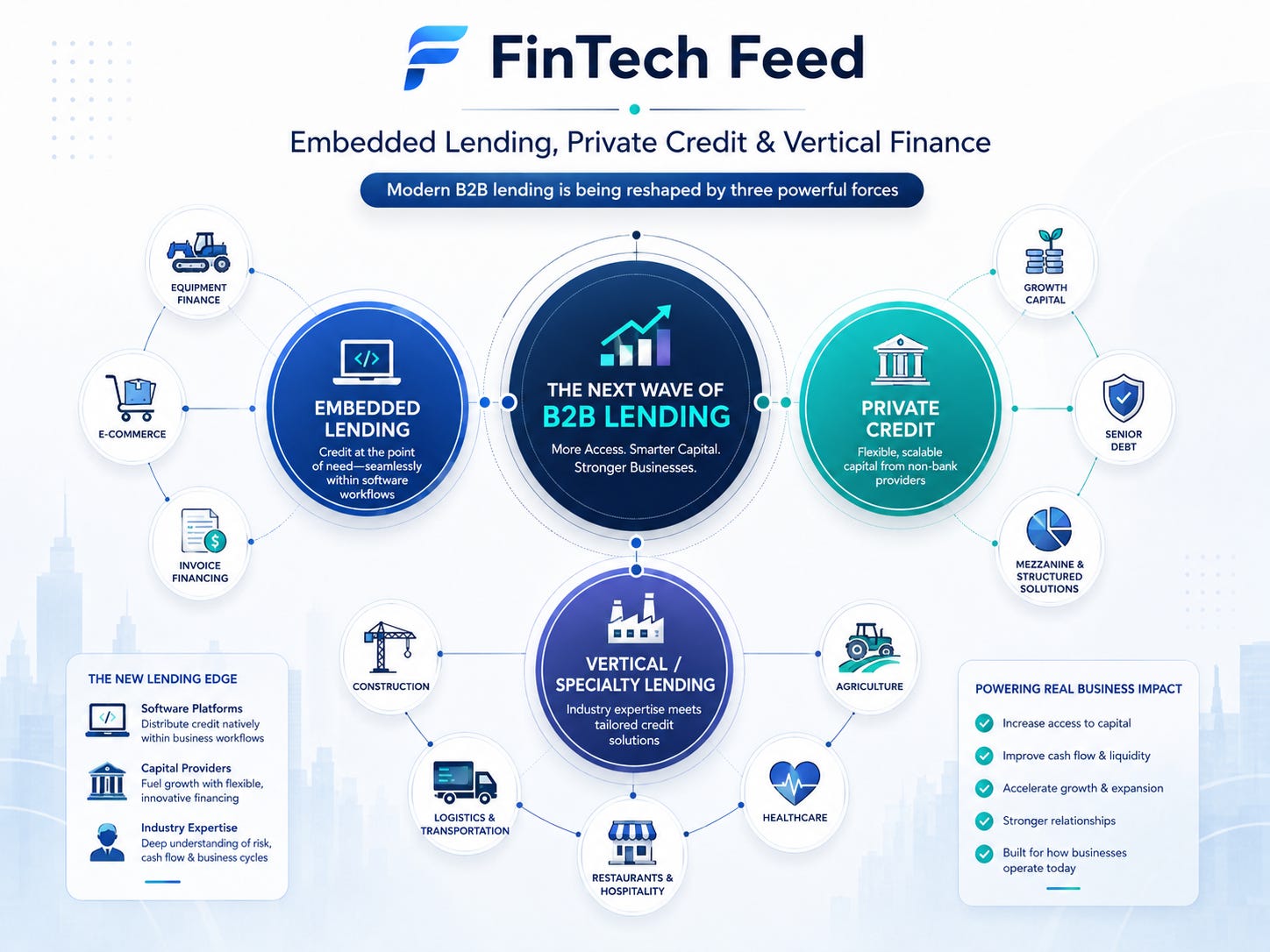

This month, we spent a lot of time focused on one of the most important — and often misunderstood — categories in financial services: B2B lending.

From working capital and equipment financing to invoice factoring, merchant cash advance, agriculture lending, and embedded credit programs, the market is moving toward more specialized lending products, more flexible infrastructure, and more thoughtful vendor selection.

Here’s a recap — and why it matters.

William M. (Founder, Director @FinTechtris)

🗓 What We Published This Month in ‘FinTech Feed’

Your Guide to the B2B Lending Ecosystem

Earlier this month, we published “Your Guide to the B2B Lending Ecosystem” — a full breakdown of how fintech infrastructure, embedded finance, and private credit are rewriting the rules of commercial lending.

For years, B2B lending was one of the quieter parts of financial services.

It was relationship-driven. Paper-heavy. Slow by design. A business owner looking for capital often had to rely on a local bank relationship, manual documentation, and weeks of back-and-forth before receiving a decision.

That world still exists.

But it is no longer the whole market.

Over the last decade, the B2B lending landscape has changed dramatically because of several forces coming together at once:

Fintech infrastructure lowered the barrier to launching lending products.

Open banking gave lenders access to real-time financial data.

Private credit stepped into areas where banks pulled back.

Embedded finance turned SaaS platforms, marketplaces, payroll tools, procurement systems, and vertical software companies into potential lending distribution channels.

The result is a B2B lending ecosystem that is larger, faster, more fragmented, and more specialized than ever before.

The newsletter was designed as a full map of that ecosystem — not just for lenders, but also for fintech operators, infrastructure companies, embedded finance platforms, banks, investors, and GTM teams trying to understand how the market works.

Read the full FinTech Feed newsletter:

https://fintechtris.substack.com/p/your-guide-to-the-b2b-lending-ecosystem

📅 What FinGTM Subscribers Got This Month

This month, FinGTM went deeper into B2B lending — not just as a product category, but as a full operating system.

The two May issues were designed to work together:

Issue #1 focused on what a modern B2B lending program needs to support.

Issue #2 focused on the vendors that can help lenders build, launch, manage, and scale those programs.

Together, they form a practical guide for fintechs, lenders, platforms, and revenue teams thinking about how to evaluate the B2B lending opportunity.

📖 Issue #1: The B2B Lending Ecosystem Guide

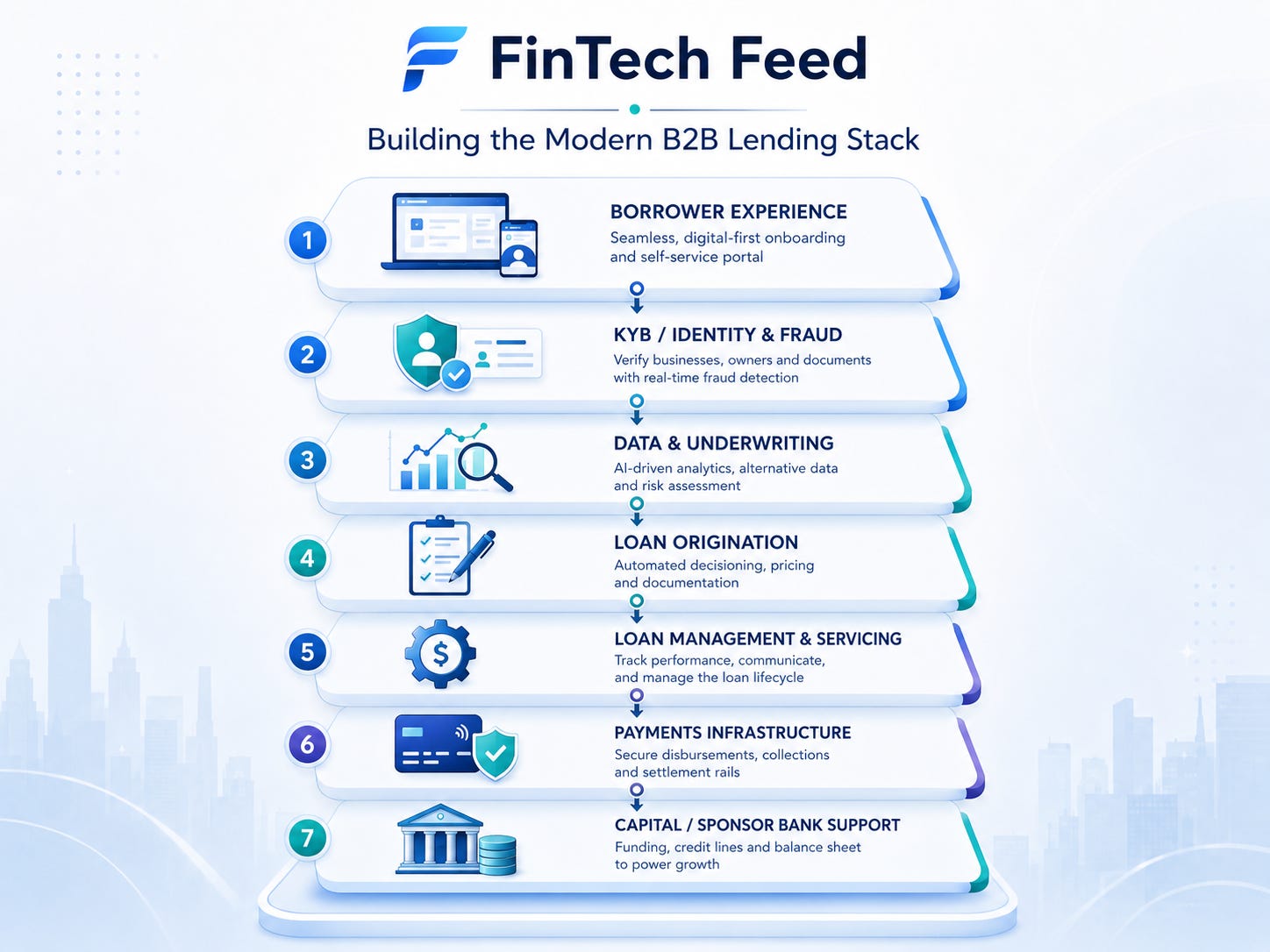

The first May FinGTM issue broke down the modern B2B lending ecosystem and the core capabilities lenders need before launching or expanding a business lending product.

The central idea: B2B lending is not one product. It is a collection of credit products, workflows, risk models, data inputs, servicing requirements, and repayment structures.

That means the first question lenders should ask is not, “Which lending vendor should we pick?”

It should be: What type of B2B lending business are we actually trying to build?

The issue covered the major B2B lending product categories, including:

Working capital loans

Merchant cash advance

Invoice factoring

Equipment financing

Agriculture lending

Embedded lending

Revenue-based financing

Lines of credit

Term loans

It also broke down the functionality lenders need across the full lifecycle:

Borrower acquisition

Application intake

Business verification

KYB/KYC

Data aggregation

Underwriting

Loan decisioning

Offer configuration

Document generation

Funding

Repayment

Servicing

Collections

Reporting

Portfolio monitoring

The issue also highlighted a major market reality:

The lenders that win in B2B credit are not always the ones with the most capital. They are often the ones with the clearest product focus, the best workflow design, and the strongest infrastructure decisions.

For GTM teams, the takeaway was especially important.

Before selling, partnering, or building in this market, you need to understand which credit products are operationally simple, which ones require specialized workflows, and which ones create the most risk if the infrastructure is not built correctly.

Read FinGTM Issue #1:

📚 Issue #2: Vendor Guide for the Modern B2B Lending Stack

The second May FinGTM issue picked up where the first one left off.

Once you understand what a B2B lending program needs to support, the next question becomes: Which vendors should be part of the stack?

This issue provided a vendor-focused breakdown across the major layers of modern lending infrastructure, including:

Loan origination systems

Loan management and servicing platforms

Decisioning and underwriting tools

Data providers

KYB/KYC and compliance vendors

Bank account and cash flow data providers

Document generation tools

Payments and repayment infrastructure

Collections and portfolio monitoring solutions

The issue placed particular focus on two major vendor categories:

1. Loan Origination

Loan origination platforms help lenders manage intake, application workflows, document collection, underwriting steps, approvals, offers, and borrower communications.

The guide explored what lenders should look for in origination vendors, including:

Configurable application flows

Business borrower data collection

Underwriting workflow support

Integrations with credit, bank data, fraud, and KYB vendors

Ability to support multiple products

Automation without losing human review controls

Clear handoff from origination to servicing

The key recommendation:

Do not pick a loan origination system based only on today’s first product. Pick one based on the lending roadmap you expect to support over the next 24 months.

A lender starting with working capital may eventually want to support equipment financing, invoice factoring, lines of credit, or embedded credit.

The wrong origination platform can slow down that expansion.

2. Loan Management and Servicing

The issue also covered loan management and servicing vendors — the systems that manage loans after approval and funding.

This includes:

Payment schedules

Interest calculation

Fees

Modifications

Payoffs

Borrower communications

Delinquency tracking

Collections workflows

Reporting

Portfolio management

Accounting and reconciliation support

This part of the lending stack is often underestimated.

The issue made a clear point:

Origination gets the loan booked.

Servicing determines whether the loan can be managed profitably, compliantly, and at scale.

For lenders offering multiple B2B products, servicing flexibility becomes even more important. A merchant cash advance, term loan, equipment financing agreement, and invoice factoring facility do not behave the same way after funding.

The vendor stack needs to support those differences.

Read FinGTM Issue #2:

📣 Why These Two FinGTM Issues Matter Together

The two May FinGTM issues were intentionally connected.

The first issue answered: What does a modern B2B lending program need to do?

The second issue answered: Which vendors and infrastructure categories help make that possible?

Together, they give lenders and fintech operators a practical framework for evaluating:

Which B2B lending products to launch first

How complex each product type is operationally

Which workflows need to be supported

Which vendors belong in the stack

Where lenders should avoid overbuilding too early

Where lenders should avoid underinvesting in infrastructure

How to think about vendor flexibility across multiple products

When a specialized platform may be better than a general-purpose lending system

This is exactly the type of content we’re building FinGTM for.

Not surface-level trend coverage. Not generic fintech commentary.

Execution-grade guidance for the people actually building, selling, partnering, launching, and scaling financial products.

🤔 Why Subscribe to FinGTM?

FinTech Feed gives you the strategic overview and industry context.

FinGTM gives you the execution playbook — the frameworks, vendor maps, templates, scripts, and tactical guidance you need to actually implement what we’re discussing.

Here’s what paid subscribers to FinGTM get every month:

✅ Two in-depth newsletters covering GTM strategy, revenue operations, fintech partnerships, infrastructure buildout, sponsor bank relationships, embedded finance, lending, payments, and more

✅ Subscriber-only chat access where you can ask specific questions about your situation and get expert responses

✅ Bonus execution content including templates, frameworks, playbooks, CRM workflows, vendor evaluation guides, and other resources you can adapt immediately

✅ Practical fintech operator guidance built for founders, sales leaders, partnership teams, product leaders, and infrastructure companies

Recent FinGTM topics have included:

Sponsor bank readiness

Why banks say no to fintech programs

Conference ROI and GTM planning

Fintech infrastructure vendor selection

Partnership economics

B2B lending ecosystem design

Modern lending stack vendors

FinGTM costs $10/month or $100/year.

For less than the cost of one lunch, you get access to tactical fintech GTM and infrastructure playbooks that can help your team make better decisions, avoid expensive mistakes, and move faster with more confidence.

🚀 Premium FinGTM: Upgrade to an Open Line of Support

For teams that want more direct input, the Premium FinGTM subscription adds:

A quarterly 1:1 call focused on your specific GTM project, fintech partnership, vendor strategy, or launch challenge

A follow-up resource with tailored guidance after the call

Access to the standard FinGTM benefits, including two monthly newsletters and subscriber chat access

This is designed for teams that want feedback, clarity, and direction right away — not just read-only content.

If you’re working through a sponsor bank process, evaluating lending vendors, building a fintech GTM motion, launching a new product, or trying to better understand infrastructure options, Premium FinGTM gives you a more direct way to get support.

Upgrade to Premium FinGTM today!

👉 Final Thought

May’s content was all about moving from strategy into execution.

B2B lending is a massive opportunity, but it is not a simple one.

The lenders and fintech platforms that succeed will be the ones that understand their product focus, choose the right infrastructure, build with compliance and servicing in mind, and avoid treating every lending category like the same workflow.

That’s the work FinGTM is here to support.

Thanks for reading, subscribing, and sharing our newsletters with your network.

See you next month!