Top Growth Levers for Fintech Programs & Apps in 2026

Why the next wave of growth is won by apps that turn users into financially active customers — moving deposits, spend, payments, savings, subscriptions, everyday transacting into one experience.

For consumer fintech, 2026 is a year of reckoning.

The early playbook — remove fees, streamline onboarding, offer a card, add early direct deposit, build a clean mobile experience — worked brilliantly when traditional banking was clunky and slow.

It produced a decade of impressive growth curves, massive user acquisition numbers, and enough venture capital to fund an entirely new sector of financial services. But it also produced something else: millions of accounts that were opened, funded once, and then quietly abandoned.

The competitive bar has risen sharply.

Traditional banks have modernized their digital channels. Neobanks are mainstream. Wallets are everywhere. The average consumer now uses multiple finance apps simultaneously — and they’re remarkably comfortable switching, splitting, and optimizing across all of them.

In this environment, customer acquisition costs for fintechs have become structurally difficult to sustain for companies that can’t convert signups into recurring revenue-generating behavior.

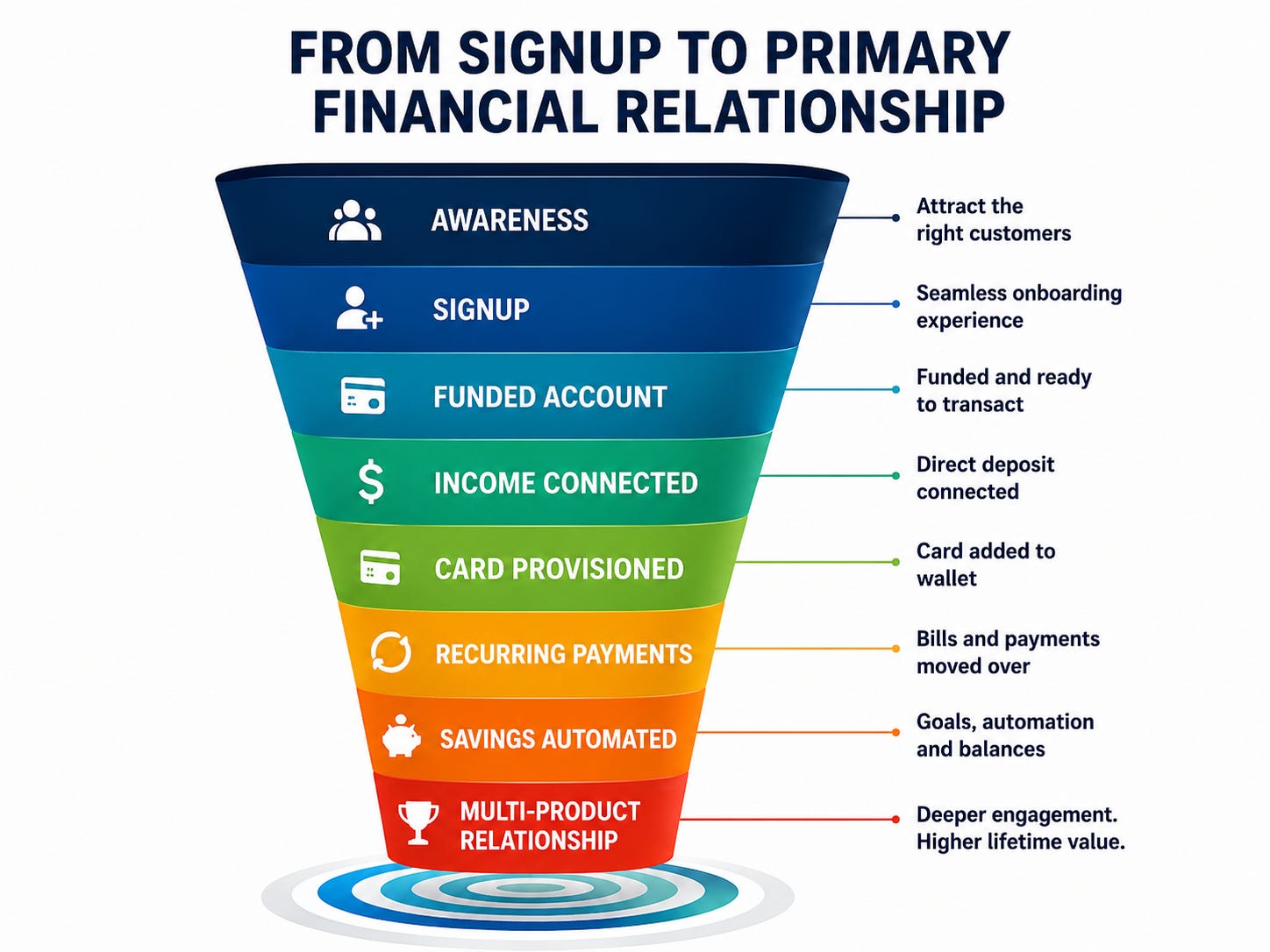

The question consumer fintech companies need to answer in 2026 isn’t “how many people signed up?” It’s “how many customers moved real financial activity into the platform?”

That means holding balances, running direct deposit, spending on the card, paying bills, moving money regularly, and adopting additional products over time — not just downloading the app, collecting a signup bonus, and staying passive.

The data tells the story clearly.

U.S. consumers made an average of 48 payments per month in 2024, with monthly payment value averaging $6,867 per person. Mobile phone payments grew from an average of four per month in 2018 to 11 in 2024, according to the Federal Reserve’s Survey and Diary of Consumer Payment Choice.

That money is moving somewhere every single day.

The growth opportunity for fintech isn’t to create new financial behavior — it’s to capture the financial behavior that already exists.

Two companies illustrate what capturing that behavior looks like at scale.

Chime reported in Q1 2026 that active members grew 19% year over year to 10.2 million, while purchase volume increased 15% to $40 billion — and credited membership tiers specifically designed to drive deeper direct deposit relationships and higher revenue per active member.

SoFi reported in Q3 2025 that total deposits had grown to $32.9 billion, with nearly 90% coming from direct deposit members, alongside interchange revenue tied to nearly $20 billion in annualized card spend.

Neither result happened because of a promotional APY or a clever onboarding screen.

Both happened because these companies designed their products around financial activity, not just account opening.

That’s the new growth equation in 2026 — here’s your 10-min crash course.

William M. (Founder, Director @FinTechtris)

Reading time: ~10 minutes

🔔 Not a Subscriber to the ‘FinTech Feed’? — sign up today (it’s free)

We curate monthly deep dives into the trends, drivers of industry growth, and initiatives that impact performance. Join 1,000+ industry professionals building the next generation of FinTech!

(For existing subscribers) It’s time to level-up GTM revenue & growth capabilities (in your company and/or career)! Upgrade to FinGTM today — a niche hub dedicated to game-changing initiatives in FinTech — from product/program design, bank sponsorship, new partnerships, sales motion enablement, growth levers, to project cycle management.

💸 Winning the Income Side: Direct Deposit at the Core

If there’s a single lever that separates a primary financial relationship from a secondary account, it’s direct deposit.

When a customer routes income into an account, the product becomes the starting point for spending, bill payment, savings, transfers, and every future product the lender or fintech wants to offer.

The account moves from a feature they happened to download to a financial hub they depend on.

The problem is that direct deposit switching is still more friction-laden than it should be. Consumers worry about payroll delays, navigate confusing employer portal experiences, and carry a quiet anxiety about what happens if something breaks mid-cycle.

For many users, the perceived risk of switching their paycheck — even temporarily — outweighs the marginal benefit of any signup incentive.

This means fintech apps that treat direct deposit setup as a settings-page afterthought are leaving their most valuable activation lever untouched.

The better approach is to treat direct deposit as a guided journey with visible progress, status tracking, employer search, fallback funding options if the first paycheck is delayed, and clear messaging about what to expect.

Citizens Bank’s work with Mastercard Open Finance demonstrated this dynamic directly — the bank found that many new account relationships stalled when customers didn’t move essential financial activity over, and embedded digital direct deposit switching into onboarding to help customers build the habits that define primary banking relationships.

The insight applies equally to digital-native fintechs: don’t make direct deposit a task.

Make it a milestone.

📚 The GTM Content Pack for Fintech/Payments/AI/ B2B SaaS Teams

For fintech founders, revenue leaders, and enterprise sellers, we also offer the FinTechtris GTM Content Pack.

This resource includes ready-to-use frameworks designed to help fintech teams accelerate growth, including:

- Enterprise fintech sales messaging frameworks

- Embedded finance launch planning templates

- Partnership outreach strategies

- Content frameworks for fintech thought leadership

It’s designed for teams that want to move faster when launching new fintech initiatives or expanding into new markets.

Explore the GTM Content Pack today!

🏦 Winning the Outflow Side: Recurring Payments as the Other Half of Primacy

Direct deposit handles the income side of account primacy.

Recurring payments handle the outflow side — and it’s the lever that most fintech apps still underestimate.

Consider what happens when a customer’s phone bill, rent payment, insurance premium, gym membership, Netflix subscription, and utility bill all flow through one account.

That account becomes functionally impossible to abandon.

The switching cost isn’t just inertia — it’s the genuine operational effort of redirecting every recurring obligation to a different institution.

That stickiness is enormously valuable, and it’s available to any fintech willing to actively help customers migrate it.

The path there is more active than most products currently support.

An app can identify recurring transactions from linked external accounts, surface which subscriptions and bills are eligible to move, provide card update tools for subscriptions that require a card number change, and create an explicit “make this your primary account” checklist that walks customers through the transition step by step.

Beyond retention, recurring payment data is also one of the richest signals for a fintech that wants to offer personalized financial insights, cash flow alerts, overdraft alternatives, or credit products.

A fintech that sees every bill knows when a customer’s cash flow is tight before the customer does — and that’s an extraordinarily useful place to be.

💳 Card Spend: Context Over Cashback

Higher cashback rates can drive short-term card adoption, but they’re not a durable strategy.

Rewards economics are expensive, they attract promo-sensitive customers who will optimize across multiple cards, and for debit-focused fintechs, the unit economics can be difficult to sustain without sufficient customer lifetime value elsewhere in the relationship.

The stronger strategy is to make card spend contextual — connected to the customer’s actual life, goals, merchants, and financial situation rather than a generic “spend and earn” mechanic.

A fintech app serving gig workers could tie card use to real-time tax savings buckets.

A student banking product could surface campus merchant offers and subscription tracking.

A family banking app could connect card spend to savings goals, allowance flows, and household budgeting.

A small business product could link every card transaction directly to bookkeeping categories, receipt capture, and cash flow forecasting.

When a card becomes part of how someone manages their money rather than just how they access it, the relationship with the product deepens in a way that a cashback rate can never replicate.

That’s the difference between a card product and a financial operating system — and the apps building toward the latter will accumulate the kind of daily usage patterns that make customers reluctant to leave.

🧾 Payments as a Habit Loop, Not a Utility Feature

Payments are where the daily habit lives.

Most consumers don’t check their savings balance every day — but they send money, split bills, pay merchants, fund wallets, and move money between accounts constantly.

McKinsey estimates that payments generated $2.5 trillion in revenue globally from $2.0 quadrillion in value flows and 3.6 trillion transactions in 2024, and describes the sector as at an inflection point across rails, programmable payments, digital assets, and platform-integrated payment models.

For consumer fintech apps, that macro reality has a direct product implication: payments are distribution.

Every payment interaction is an opportunity to deepen the relationship, surface a new feature, and create another reason for the customer to open the app again tomorrow.

Cash App illustrates the power of building a payments ecosystem rather than a payments feature.

The product combines direct deposit, a debit card, savings, peer payments, Cash App Pay, stock trading, Bitcoin, and Afterpay within a single experience — and the compounding logic is intentional.

A peer-to-peer payment leads to card spend.

Card spend leads to savings roundups. Savings lead to investing.

A merchant payment leads to a future personalized offer.

Each interaction creates the context for the next one, and the network of behaviors builds a relationship that’s far stickier than any individual feature could achieve.

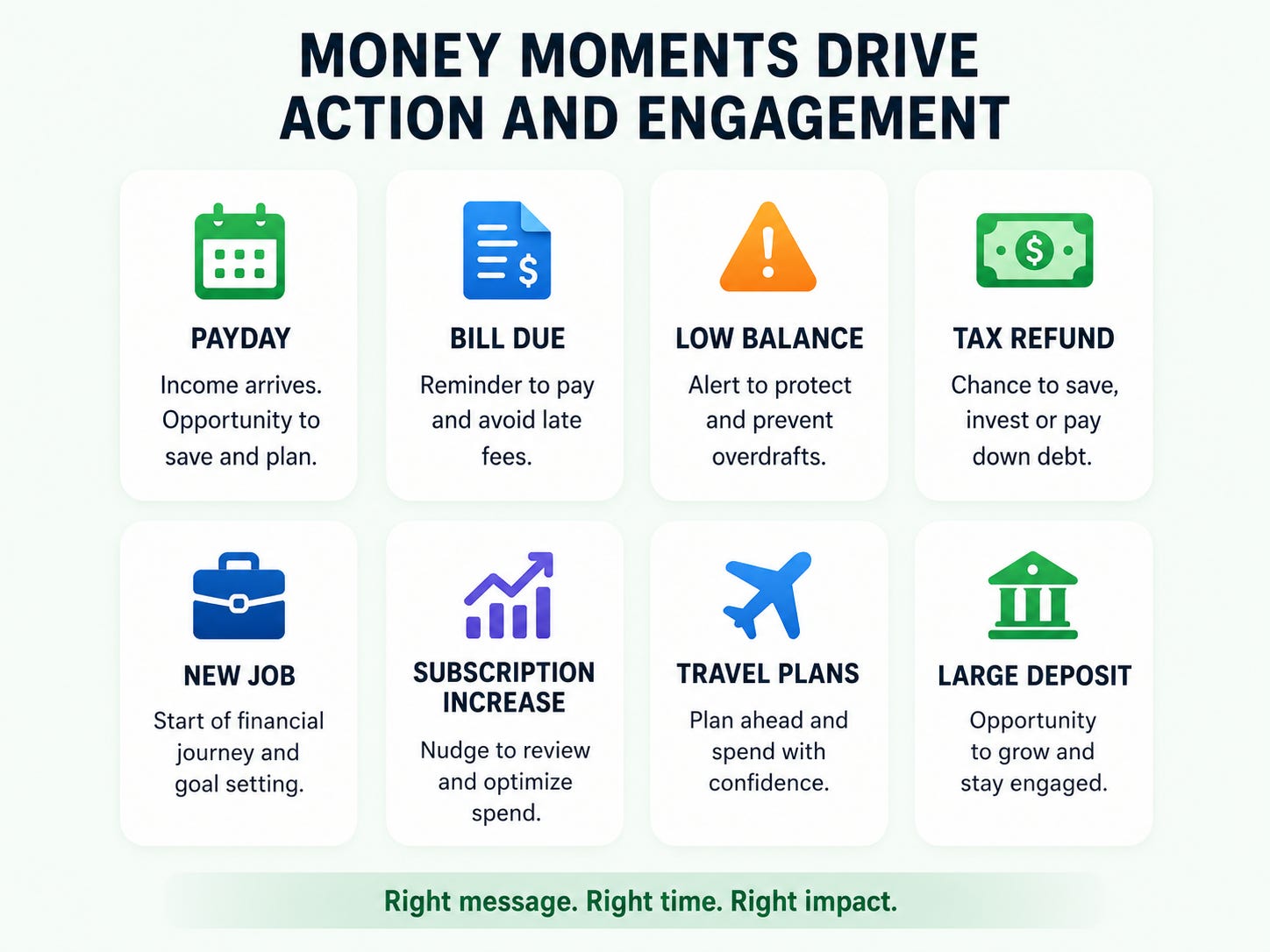

💰 Money Moments: Timing Is the Underrated Variable

The best growth strategies in fintech aren’t generic.

They’re triggered by moments — the specific points in a customer’s financial life when they’re most likely to take action because something meaningful is happening.

A first paycheck arriving creates an opening for savings automation.

A tax refund landing creates an opening for an emergency fund.

A large bill appearing creates an opening for cash flow tools.

A low balance alert creates an opening for overdraft alternatives.

A subscription price increase creates an opening for a spending review.

These moments carry urgency and context that generic product promotions simply can’t replicate.

Fintech apps that understand their customers’ money moments can shift from broadcasting features to delivering genuinely timely interventions — “your paycheck arrived, want to move 10% into rent savings?” rather than a weekly push notification about APY.

ABA Banking Journal has noted that digitally mature financial institutions are increasingly using data and marketing capabilities to proactively guide customer engagement rather than waiting for customers to initiate.

For fintech apps with modern data infrastructure, that capability is even more accessible — the app is already in the customer’s pocket, the transactions are already being captured, and the moments are already visible.

The question is whether the product is designed to act on them.

📣 Savings: Building Balances Through Automation and Purpose

A competitive APY can attract deposits. It can’t always retain them.

When another app offers a higher rate, money moves — and the customers most likely to chase yield are the ones who never developed a deeper relationship with the product in the first place.

The more durable deposit strategy combines reasonable economics with automation, goal orientation, and emotional relevance.

Savings that are connected to a specific purpose — a rent cushion, a travel fund, a tax bucket, a car repair reserve, a holiday budget — are harder to move than savings that are simply parked for yield.

Customers feel the loss of pulling money from a goal they’ve named and visualized in a way they don’t feel when moving generic cash from one high-yield account to another.

Cash App has built this insight into its product model.

The platform offers a separate savings balance funded through the Cash App balance, linked debit cards, direct deposit, and automatic roundups on card purchases — a combination that turns everyday financial activity into savings progress without requiring a separate decision each time.

The broader playbook for fintech apps is to make savings automatic, give it a name, make it visible inside the product, and connect it to financial behavior that’s already happening.

Savings automation that runs in the background builds balances in a way that asking customers to manually transfer money never will.

📈 Credit and Membership: Deepening the Relationship

Credit products are one of the most powerful ways to deepen a fintech relationship — and one of the easiest ways to damage it.

The design question isn’t whether to offer credit.

It’s whether the credit product is built to serve the customer’s actual cash flow situation or to extract value from it.

The opportunity is real: customers often need short-term liquidity, credit building, overdraft alternatives, secured credit, small-dollar loans, BNPL, or paycheck-linked advances. But the product design determines whether those offerings strengthen or strain the relationship.

Fintech apps with direct deposit data, recurring payment history, and consistent account activity have a genuine underwriting advantage over cold credit applications — they can offer cash flow-informed credit products that are better matched to borrower reality than a credit score alone would support.

Credit should be designed around customer behavior and repayment ability from the beginning, not bolted on as a revenue layer after acquisition.

Membership tiers represent a different kind of deepening — one that creates recurring revenue while giving customers a reason to consolidate financial activity.

The key is building tiers around behavioral milestones rather than access fees.

Robinhood grew Gold subscribers 36% year over year to 4.3 million in Q1 2026, while total platform assets rose 39% to $307 billion — a result that reflects how membership can anchor a broader product relationship.

Chime has made explicit that its membership tiers are designed to drive deeper direct deposit relationships, more product usage, and higher average revenue per active member.

The model works when the tier feels like a reward for engagement rather than a toll for access: set up direct deposit to unlock premium features, maintain a balance threshold to unlock higher limits, adopt savings automation to unlock financial coaching.

That design turns product engagement into a self-reinforcing growth loop.

📲 Embedded Distribution: Getting Outside the App Store

Consumer fintech acquisition is expensive when everyone is competing on the same paid social, referral, and search channels.

Those channels can work, but they rarely create durable competitive advantage — especially as the neobank market matures and customer acquisition costs for generic account products remain stubbornly high.

The stronger acquisition strategy is embedded distribution: placing the financial product inside an existing workflow, community, employer relationship, marketplace, or vertical platform where customers already have intent and financial activity is already happening.

A payroll platform offering earned wage access or banking reaches workers at the moment of income.

A gig platform offering income accounts and tax savings reaches contractors exactly when they need those tools.

A creator platform offering cards and instant payouts reaches creators at the moment they’re receiving money they’d like to manage.

A student platform offering banking and credit building reaches a customer at the beginning of their financial life.

The common thread is that embedded distribution converts financial need into product adoption without requiring a customer to seek out a new app.

The product appears at the moment of utility, which tends to produce higher activation rates, higher balance attachment, and lower churn than customers acquired through promotional channels who arrived without a specific financial motivation.

📒 Want the Playbooks Behind Fintech Growth?

If you enjoy the insights in FinTech Feed, you may also want to explore FinGTM, our premium research publication focused on the go-to-market strategies behind successful fintech companies.

FinGTM dives deeper into topics like:

- How fintech companies secure sponsor bank partnerships

- The infrastructure decisions that determine whether fintech programs succeed or fail

- GTM frameworks used by top fintech revenue teams

- The playbooks behind embedded finance launches

FinGTM subscribers receive two in-depth newsletters per month, along with opportunities to submit questions and receive expert guidance on fintech strategy.

🤝 Trust as a Growth Variable

Trust is a growth lever — though it rarely appears on acquisition dashboards.

Many fintech teams still classify fraud prevention, dispute resolution, and customer support as cost centers to be managed rather than capabilities that directly affect retention, referrals, and partner confidence.

That framing misses how customers actually think about their primary financial relationship.

A customer will not move their paycheck, savings, card spend, or recurring bills into an app they don’t trust. And trust is forged or destroyed not during the happy path, but during the moments when something goes wrong: a fraud claim, a payment dispute, a paycheck delay, a card issue.

Cash App’s 2025 product releases made this connection explicit, emphasizing features like Security Lock, Cash PIN, biometric authentication, instant card locking, 24/7 customer support, and scam reimbursement policies as part of a coordinated product strategy — not a compliance obligation.

The logic is sound.

Customers don’t separate product experience from trust experience.

A single unresolved fraud claim can undo months of positive engagement.

In 2026, fast dispute handling, transparent security controls, and human support for high-stress financial issues aren’t just table stakes for compliance — they’re among the strongest retention tools in the product.

📚 The Multi-Product Path: Sequence Matters More Than Breadth

The most successful consumer fintech apps grow by expanding from an initial wedge into a broader financial relationship. But the sequencing matters as much as the product selection.

Introducing every feature on day one creates cognitive overload and dilutes the activation focus that actually drives early habit.

The more effective model is to create a natural expansion path where each product deepens the relationship established by the last.

A customer with direct deposit is ready for savings automation.

A customer with savings is ready for investing.

A customer with consistent income is ready for a credit builder product.

A customer with recurring card spend is ready for personalized merchant offers.

A customer with bill pay is ready for cash flow forecasting.

SoFi has been explicit about this logic in its “Financial Services Productivity Loop” — the idea that a broader product suite drives more members, more product adoption, and stronger unit economics as the relationships compound.

In Q3 2025, SoFi reported 905,000 new members, 1.4 million new product additions, 37% growth in financial services products, and annualized revenue per product of $104, up 29% year over year.

The lesson isn’t that every fintech should become SoFi.

It’s that every fintech needs a product expansion path — because the first product gets the customer, the second builds habit, the third improves economics, and the fourth creates the kind of defensibility that makes the relationship genuinely hard to displace.

📚 How ‘FinTech Feed’ Helps You Stay Ahead

If you’ve made it this far, you already understand something important:

This industry is getting more complex.

And the stakes are getting higher.

That’s exactly why FinTech Feed exists:

—> Monthly insights on what’s happening across fintech

—> Designed to keep you informed and ahead of trends

—> No cost for access

👉 Subscribe today!

📊 The Metrics That Matter

As financial activity becomes the true measure of fintech growth, the metrics teams track need to evolve accordingly.

Signups, downloads, and monthly active users tell an incomplete story — they don’t distinguish between a customer who moved their paycheck and a customer who opened an account, claimed a bonus, and never returned.

The metrics that actually reflect account primacy and revenue-generating activity tell a different story:

Activation and funding: Funded account rate, direct deposit attach rate, card activation rate, wallet provisioning rate.

Financial activity depth: Average and median deposit balance, monthly card purchase volume, transactions per active user, recurring payment migration rate, bill pay adoption, peer-to-peer payment frequency, cash-in and cash-out volume.

Product expansion: Savings automation adoption, credit product adoption, multi-product adoption rate, revenue per active user.

Retention quality: Retention by financial activity cohort, fraud loss rate, complaint rate, support resolution time.

Segmenting these metrics by acquisition channel is just as important as tracking the numbers overall.

A user acquired through an employer relationship, an embedded partner, or a community referral often behaves meaningfully differently from one acquired through paid social — higher balances, stronger direct deposit attach, lower churn.

The right acquisition channel isn’t necessarily the cheapest.

It’s the one that produces the highest-quality financial activity over time.

🚀 What This Means Across the Industry

The same core principle plays out differently depending on where an organization sits in the ecosystem.

For fintech startups, the priority is proving that customers will move meaningful financial activity into the product — not just create accounts. Activation mechanics, direct deposit conversion, and card spend per active user matter more than gross signups as early signals of product-market fit.

For digital banks, the priority is account primacy: making direct deposit, bill pay, recurring payment migration, and card spend easier and more compelling than staying split across legacy institutions. The competitive advantage isn’t product features — it’s the friction removed.

For enterprises launching embedded finance programs, the priority is tying financial products to existing customer workflows rather than asking customers to adopt a separate banking experience. The financial product should appear inside the context where the customer already has intent.

For financial institutions, the priority is defending deposits and payments by matching the activation ease, direct deposit switching tools, and data-driven engagement capabilities that fintech competitors have built. Institutions with existing customer relationships have a trust advantage that’s worth protecting with modern tooling.

For vendors selling into fintech and banking teams, the priority is helping operators demonstrate measurable outcomes — not just feature delivery. Activation rates, retention by cohort, direct deposit attach, and revenue per active user are the metrics that matter to buyers, and vendor value propositions should be built around moving them.

💻 The Apps That Win Will Become Financial Routines

The next generation of consumer fintech growth won’t come from louder promotions or higher APYs.

It will come from becoming part of how customers run their financial lives — woven into the paycheck, the bills, the everyday spending, the savings goals, and the moments when financial decisions need to be made.

That requires more than any single feature can deliver.

It requires product design that guides activation, data infrastructure that enables timely intervention, payments and savings mechanics that create automatic habit, credit and membership models that reward engagement, embedded distribution that reaches customers at the moment of need, and trust infrastructure that makes customers willing to move their real financial life into the product.

The fintech apps that understand that full journey — and build toward it deliberately — are the ones positioned to capture the financial activity that will define the next wave of consumer fintech growth.

FinTech Feed by FinTechtris breaks down the trends shaping fintech, banking, payments, lending, embedded finance, and financial infrastructure. For deeper operator playbooks, upgrade to FinGTM for tactical resources built for fintech founders, revenue leaders, product teams, partnership teams, and financial services executives turning market insight into execution.